Adulting 101

Managing your money for the short and long term

You’ve reached adulthood — perhaps long ago — but are you a financial adult?

Becoming a financial adult isn’t just about earning enough to support yourself, although that’s certainly a good start. It’s also about practicing financial habits that will give you greater peace of mind and ideally more choices in life.

To gather a few tips on what it takes to become a financial adult, we turned to Pacific University Assistant Professor Laura McNally, who teaches accounting at the College of Business and once ran her own Certified Public Accountant (CPA) practice.

We also consulted Pacific alumna Noel Pacarro Brown MAT ’05, a financial advisor and senior investment management consultant at The Pacarro Group at Morgan Stanley, a Honolulu-based, multi-generational wealth management team.

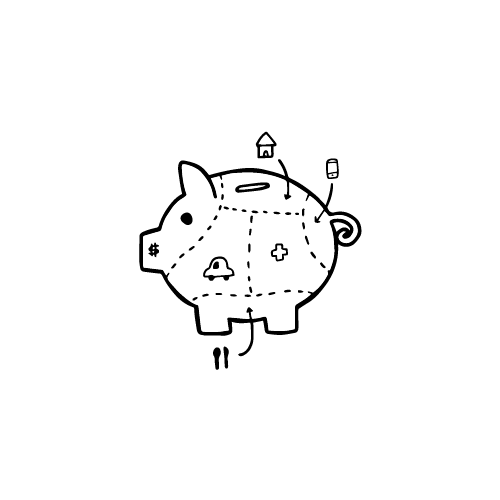

Make a Budget

Coming up with a budget, doesn’t necessarily mean you’ll have to give up your daily trip(s) to Starbucks.

But making a budget can keep you from spending more than you earn.

McNally says the first order of business is figuring out how much you spend every month.

Look at your bank statements, receipts and other financial documents to get a sense of how much of your money is going toward fixed expenses (rent, groceries and gas, for instance) versus discretionary expenses.

Don’t forget to set aside some money for unanticipated things, like car repairs.

Once you know how much you need for your fixed costs, you can begin to think about how to handle your discretionary income. Set aside some money for fun stuff and for savings and debt repayment.

“A budget doesn’t need to be too tight or uncomfortable,” McNally said. “But it does give you a sense of how much you need to earn to cover your expenses, and thus what type of job you can accept. It can also help you to sleep better at night, knowing you have money set aside for a big bill that you weren’t expecting.”

Save for emergencies & retirement

Allocate money in your budget for emergencies, such as a job loss or unexpected medical bills, and retirement. Generally, your emergency fund should cover three to six months of expenses.

Having money set aside for emergencies not only gives you peace of mind, but more freedom to do things like quit a job you dislike.

“It gives you a ton of confidence knowing that if you are in a job that you don’t love, you have the freedom to move on,” said Pacarro Brown.

The sooner you start saving for retirement (even in small amounts), the more time your money has to grow. Each year’s gains generate their own returns the following year, a lovely phenomenon known as compounding.

“The power of compounding is the best financial magic there is,” said Pacarro Brown. “Time is on your side when you are young, so the sooner you start to save, the better off you are.”

Use Credit Wisely

You may want to use credit cards for the points and other perks, but be sure to pay the balance in full each month.

“I never buy anything on credit unless I can pay it off because the interest rates are usually outrageous,” said McNally.

If you are already in debt, strive to pay off your high-interest debt first. While it’s important to pay off lower-interest debt, such as student loans, try to also set aside some money for emergencies.

Become a Knowledgeable Investor

Get to know the basics of investing, especially if you are putting money into a 401(k) plan or some other kind of retirement savings vehicle.

Once you have identified some investment funds, you may want to keep digging to get a sense of whether their holdings align with your values, said Pacarro Brown.

“Know what you own, recognizing that every dollar you spend is an expression of your values,” she said. ■

This story first appeared in the Winter 2017 issue of Pacific Magazine. For more stories, visit pacificu.edu/magazine.